Consolidation over the past decade has effectively transformed the broker-dealer landscape, with the number of FINRA-registered firms dropping by nearly 25% since 2004. The same forces and competitive threats that are driving consolidation among broker-dealers are also at play in the current environment of Offices of Supervisory Jurisdiction, leading to an evolution in the way OSJs do business in a highly competitive climate.

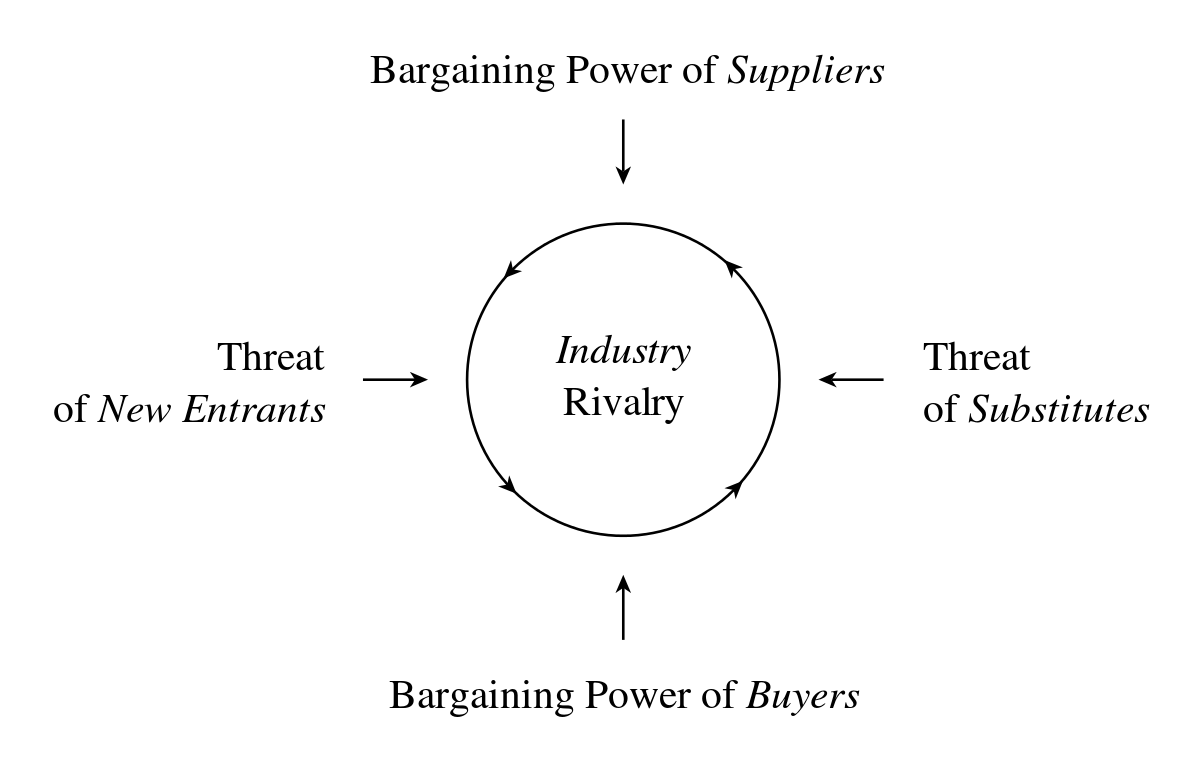

In the past, the SWOT rubric might have been adequate to explain the changes in the role and value proposition of the traditional OSJ in the wealth management chain, but a more nuanced approach using Porter's Five Forces reveals deeper insight.

Michael Porter, the Harvard Business School economist, developed his "Five Forces" framework as a way to explain, at a micro level, the external forces that affect the way a business serves its customers and makes a profit. Under the framework, a company that can adapt its core competencies and business model to achieve higher than average profits within its industry can survive changes in market forces even in an "unattractive" industry, which Porter defines as one that is approaching "pure competition," where all available profits within a given industry are driven down.

The framework describes three horizontal threats (Threat of New Entries, Threat of Substitutes, and Threat of Existing Industry Rivalry) and two vertical threats (Bargaining Power of Suppliers and Bargaining Power of Buyers) as the chief forces shaping the competitive strategies paradigm. Each can be evaluated and applied within the OSJ industry to explain the evolution in the traditional OSJ model over the past decade.

While the broker-dealer industry is consolidating, more advisors are moving beyond a captive channel and into an independent role. This opens up space for the OSJ to innovate and expand its offerings beyond simple supervision, licensing, and compliance to include a full menu of fee-based practice management services that are driving top line revenue.

The Super OSJ model is an example of this phenomenon. A 2016 survey by AssetMark revealed that Super OSJs, or "Business Builder" models, are not only the fastest growing in terms of new entrants, but also in terms of increasing revenue far more effectively than their traditional OSJ counterparts. Super OSJs showed a 32% revenue growth rate over three years compared to just 12% growth for the traditional model.

When independent advisors begin aggressively recruiting to expand their practice, it's only natural to consider the option of becoming an OSJ as a path toward growth. Pete Bush of Cetera Advisors was working under an OSJ when he decided it made more sense financially to start his own OSJ.

After a few years in the three-partner, six-advisor practice, a partner at Cetera advised him to pursue profitability through aggressive growth. So he did, and five years later, Bush's Horizon Wealth Management oversees $1 billion in assets and his OSJ added over $6 million in top-line revenue.

In Porter's framework, the Threat of Substitution refers to existing products outside a company's particular industry that buyers could substitute for the company's product. For example, water is a substitute for Pepsi, while Coke would be a competitor.

In the OSJ industry, the threat of substitution comes from captive wirehouse channels, especially in the post 2016 Department of Labor fiduciary rule under ERISA. It is undeniable that the regulatory burdens have increased exponentially, making it more expensive and perhaps less attractive for financial advisors to transition from a wirehouse to an independent role.

And the complex, expanding, and ever-changing regulatory and compliance requirements make it undeniably more costly for independent advisors and small broker-dealers to hire in-house compliance officers and their accompanying high annual fixed costs.

The super OSJs are essentially substituting for the smaller broker-dealers. The dynamics have shifted radically under the consolidation trend. Currently, the top 10 largest independent broker-dealers handle about 65% of the available industry business, with the remaining firms battling it out for the leftover 35%. Some industry analysts expect that to hit 80-20 or even 90-10 over the next decade.

Perhaps nowhere else is the pressure of consolidation more acutely felt as a competitive threat than in the bargaining power of advisors. Super OSJs are helped tremendously by the fact that smaller, independent brokers are throwing in the towel under shrinking margins and expanding compliance requirements.

Economies of scale allow the larger OSJs to provide a plug-and-play environment where practice building services (such as customer relationship management (CRM) technology and other productivity enhancers, marketing, and practice management options) are available in addition to supervision, while still maintaining solid payouts.

The dynamic that is playing out with investors, who demand more from their financial planners and wealth managers due to increasing competition and a host of new investment technologies, is also playing out between advisors and their broker-dealers and OSJs.

It's no longer enough for OSJs to provide basic supervision and compliance services. Reps want a competitive menu of operational support options with the flexibility to bundle services in exchange for a slightly lower payout. Few OSJs operate under a strictly outsourced framework where services are selected and paid for a la carte.

Private Advisor Group (PAG), an OSJ for LPL Financial, has $18 billion in brokerage assets, 12 compliance officers, and over 500 advisors. They recently initiated an aggressive campaign to identify retiring advisors in their service area whose clients will need a new home.

PAG is proactive in presenting succession-planning options to the soon-to-be-retired advisors, connecting them with active PAG advisors during the course of invitation-only educational events and seminars. In each of the pilot program solicitations, PAG advisors acquired at least one new practice.

These are the types of value-added services the most successful advisors will expect, if not demand, from their OSJs as they exert their buying power in a competitive threat environment. The AssetMark survey results bear this out: The average AUM per advisor in the "Business Builder" super OSJ model was $38 million with average annual revenue of about $280,000 versus just $12 million in AUM and $118,000 in annual revenue for the traditional OSJ model.

Under Porter's framework, suppliers of expertise have power when there are few substitutes or when there is a high degree of differentiation. Under the evolving OSJ environment, the super OSJ model itself is a competitive threat to the traditional OSJ.

The AssetMark survey revealed that segmentation is already raising the stakes for traditional OSJs, which must compete for the most successful and productive advisors. In 2016, the traditional OSJ model accounted for just 40% of the emerging business models while super OSJs and hybrid models serviced 60%.

Those OSJs who are able to extend the services offered by a broker-dealer and simplify practice management for the advisors are able to recruit and retain the most motivated advisors. OSJs that are able to offer better options in terms of affiliation options, branding, compensation, recruiting, technology, and operational services are a distinct threat to those operating in the traditional OSJ space.

These new OSJ models are more attractive to advisors and, as a result, exert pressure on traditional OSJs and smaller firms that may not be able to afford the costs of supervision in a restrictive and evolving regulatory paradigm.

Innovation and competitive strategy are major factors in determining industry competitiveness for OSJs. There is no doubt that the super OSJs have embraced innovation to make themselves more attractive to advisors. Some, for example, are operating in niche markets, such as 401(k) plans. Others emphasize value-added services that move beyond compliance support into coaching, mentoring, and networking.

Bill Morrissey, director of the Independent Advisor Services group for LPL Financial, says that OSJs whose only value proposition is supervision are becoming an anachronism. "The two things that most advisors willingly pay a premium for is increased efficiency, increased productivity and help growing their business," he said.

Larger enterprises have the bandwidth to offer these additional services and still produce higher payouts. Eric Schwartz, chairman of Cambridge Investment Research, said that the competitive industry environment hurts "less sophisticated OSJs who (sic) do not offer as much value" and have less wiggle room around the margins. Broker-dealers, he notes, offer advisor payouts of about 70% to 90% depending on their business model, while super OSJs are offering 92% to 95%.

The increased complexities of new regulation, particularly the DOL fiduciary rule, will also put pressure on smaller OSJs that lack the sophistication to help advisors thrive in this new regulatory environment.

In 2006, broker-dealer Cambridge Investment Research had five OSJs accounting for about 10% of its sales and generating about $20 million in revenue. Last year, the figure had jumped to 23 super OSJs generating $200 million in revenue and 30% of the Cambridge's sales.

OSJs that offer their advisors practice management, marketing, technology and leadership support have a leg up in the highly competitive OSJ industry. OSJ executives who embrace fin tech and business intelligence tools, such as Truelytics, to get a detailed understanding of how their network practices are performing, are better positioned to offer the type of insight and services necessary to recruit top advisors. As Cambridge's Schwartz noted, there is a lot happening right now in the wealth management industry, and advisors need the right tools and information because they "don't want to get lost in the shuffle."

You May Also Be Interested In Reading: The Evolution of the OSJ Business Model